At some point you want to make sure you cover the legal side of your startup. Set up the legal entities, split the equity over the team, sign that big customer or investment deal, and go conquer the world. A good legal and tax foundation will save you from a lot of headaches down the road. It pays off to study a bit of legal and tax matter before you incorporate your business.

This post creates a blueprint for a high-tech or software startup that is based on creating IP and needs external investment to pull that off. And not much more to keep things simple. No tax-evading Panamanian mailbox schemes here (“brievenbusfirma”). I’ll stay far away from these. Oh, and as (especially) tax rulings are different in every country and my experience does not cover the whole world, I’ll focus on The Netherlands. And use the Dutch terms in parentheses.

In setting up a new venture, you need to make sure you are surrounded by a team of advisors. Yet as each covers their domain of expertise, you are the one that needs to pull it all together. At the risk you can’t see the wood for the trees.

How do the advisors help you?

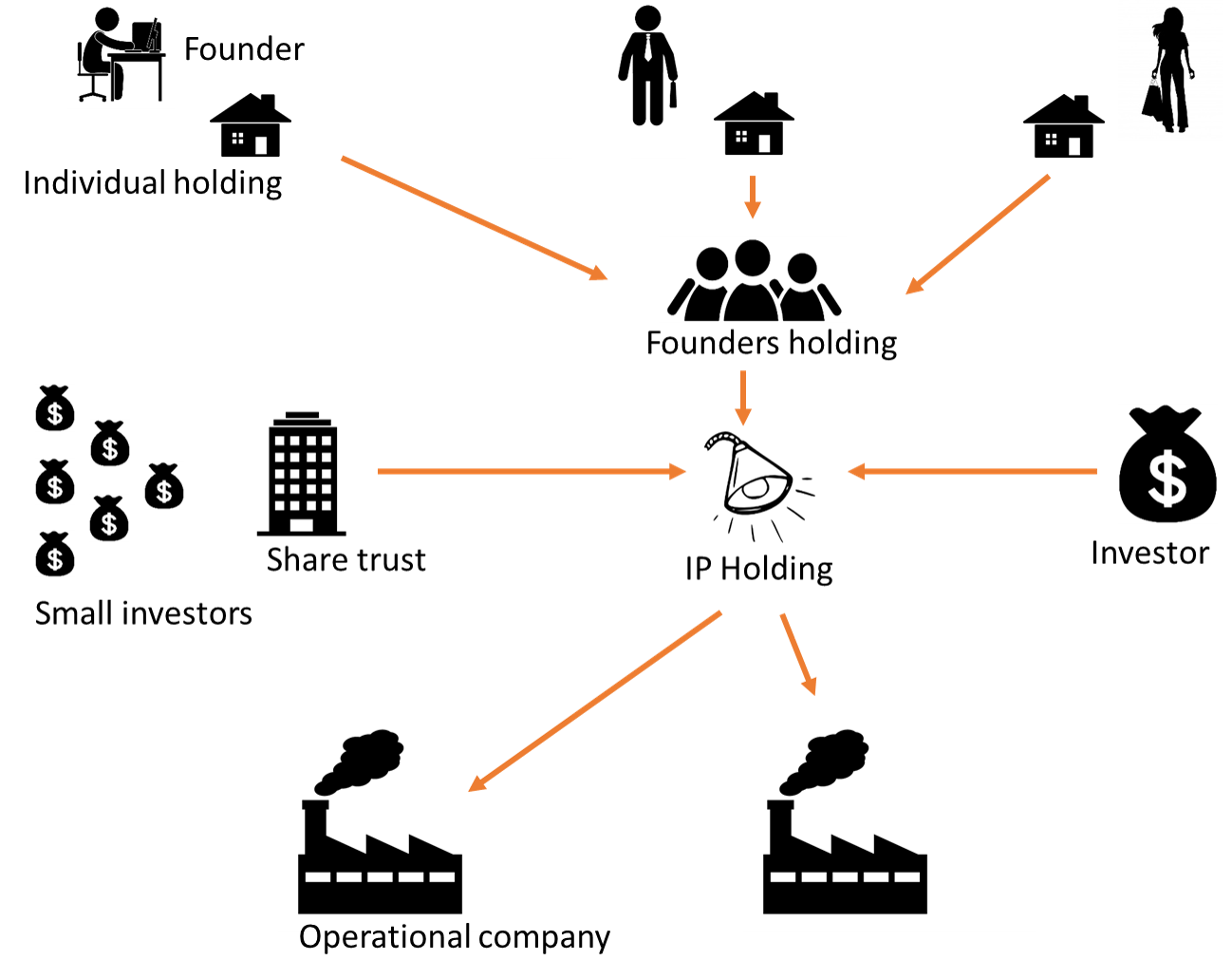

The figure shows the rough setup. I’ll walk over the entities top-down.

No caveats here. Get an online accountant to keep things afloat and cheap.

You can decide to work via your holding for the main company instead of being directly employed there. You then become the single employee (“DGA”) of your holding and invoice a management fee to every company you work with. Easier than being employed by multiple companies.

The inflow of management fees allows you to tinker with all kind of tax benefits: mortgage, pension, lease car, or deduct costs. Knock yourself out. In most cases you can even avoid paying social security for employee’s insurance, making your startup more cost effective.

If you run an innovative startup, chances are your startup can apply for some kind of government, regional, or EU subsidy. But as you now are a 3rd party contractor to the main company, most subsidies don’t or only partly subsidize 3rd party work, so beware.

An exception is the WBSO/RDA subsidy. In this case you can apply subsidy for yourself as employee of the holding, linked to the innovation done in the main company. Your holding now benefits from the subsidy, not the main company. Not every shareholder will like that though. On the positive side, you can optimize the amount of subsidy by setting smartly choosing your own salary (the level of subsidy is based on all past salaries paid out in the entity).

Caveats?

As you are the single employee and owner, the tax authority demands you pay yourself a minimum wage (“minimum DGA loon”). The guideline is currently €44k/year, but if the tax authority feels the wages in your line of work are much higher, you might be held hostage to a much higher pay grade. On the other hand, Dutch government has recently stated that for startup situations, you can bring this down to Dutch minimum wage at approx. €20k/year.

The ties your holding has with the main company should have no signals of a hidden employment relationship (“verkapte arbeidsrelatie”). Even with a management fee construct, you may be seen as employee of the main company (“materieel in dienstbetrekking”). The government currently turns a blind eye to this (“wet DBA”), so you are seemingly safe until 2018. In addition, when your setup exempts you from mandatory payments of employee’s insurance, the government will be even more flexible. Also from 2018 onward.

As a general rule, if there is a chance that others (co-founders, investors) can kick you out of the company, your startup has to pay employee’s insurance.

The only way to prove you can’t be kicked out, is to make the case you are are critical to the company as a founder:

So tough luck. In case you cannot pose the above, the main company will have to pay the employee’s insurances (“premie werknemersverzekeringen”) for your management fees or salary. That amounts to roughly ₤7k to €8k per year per employee in the IT business.

A single founders entity may also help you too, as you can negotiate that warranties and other scary constructs in the investment agreement are fended off to the holding instead of to you personally. Also, uniting the founders as a single voice at a shareholders meeting or investment negotiation may give some leverage.

High-tech, IP-heavy companies need lots of investment. If you plan to do many investment rounds, your individual share held by your holding may water down to below the magical interest (“aanmerkelijk belang”) limit of 5%. In that case you pay corporation tax over any dividend paid out and capital gain realized. If you combine forces with your co-founders in a founders holding, chances are the combined ownership floats well above 5%.

Caveats, anyone?

Not all startup marriages succeed, so plan for a graceful exit when a founder leaves. A good leaver/bad leaver clause in the founders holding makes sense to recoup shares for a replacement.

Nowadays there are alternative options to let others benefit from your business successes that are worth considering:

While SARs have nothing to do with the share capital, they do eat up part of the profit in an exit scenario. Hence, you need full shareholder approval for the SAR agreement. But as they are not directly related to shares, you can hand these out to, say, your mother in law. Without the risk she’ll ever turn up and vote against you at your shareholders meeting.

SARs are nowadays taxed as income (“box 1”). So no tax-saving stunts to be had here, alas. For stock options, you can devise a vesting scheme where you exercise the options long before the company valuation goes through the roof—effectively transferring taxation from box 1 to shares in the more favorable box 3.

Caveats!

With a STAK, the participants hold no individual shares and hence you don’t need them for signatures on follow-up investment rounds etc. But take care to really avoid having to get signatures. For instance, it may be wise to regulate a system where the participants wave their pre-emptive rights (“afzien van voorkeursrecht”) in advance. When you are in a hurry to close an investment, you simply do not want to chase a signature from a participant that just went off kayaking the Beriman river in Papua New Guinea.

Caveats?

Investors are of course smart enough to buy into the holding, instead of investing in a subsidiary that can vanish into thin air. So don’t even try to trick them. Yet do watch out for legal paragraphs in bank loans and partner contracts that try to fish for the IP through the subsidiary all the way back to your holding.

You can (and many will) have multiple operating companies to separate businesses from each other and spread the risk. For example a service company to provide services and training and separate companies for product X and Y. Each of these can then be sold independently while the IP remains with the holding.

Caveats?

Typically the risks do not outweigh the benefits of setting up a fiscal unity for VAT (“fiscale eenheid BTW”). Watch out here. You just don’t want to run the risk of a VAT claim hitting your precious IP.

It does make sense to create a fiscal unity for the corporation tax (“fiscale eenheid VPB”). The fiscal unity does go against the idea of spreading risk. But you only make a loss in developing the technology at first. So the risk of a claim on corporation tax in the early days is much lower. Another downside is that the profits of all entities are added up for the corporation tax, and thereby will hit the higher 25% tax rate (“schijf”) earlier than if filed for each entity individually.

On the subsidy level, don’t forget to account for the Innovation Box when setting up your startup structure. The innovation box effectively taxes innovative income at a mere 5% corporation tax. Although the Innovation Box only becomes truly interesting when you get to tax paying mode, be prepared. A good foundation will make it easier to apply for the Innovation Box once the money flows in. In this respect, think of earmarking expenses and turnover from day one.

So how do you get the investment dough from the holding to the subsidiary, and the customer payments back to the holding? Simple. The holding licenses the IP to the company. Say the company pays 10% of its profit for the use of the IP. The holding then loans the company its investment money to develop the IP.

You do want to use a loan instead of paying a share premium (“agiostorting”). Why? If things go south, the holding has a claim (“opeisbare schuld”) on the subsidiary for the loan. In case of a share premium, that money is gone. Also, it is easier to pay off the loan than to pay out dividend as the latter requires a complex calculation to check if you are legally allowed to do so (“uitkeringstoets bij dividenduitkering”). Furthermore, if the bank and investors let you, for example, you can create a (second) right of pledge (“pandrecht”) for the loan.

Plenty of caveats

Make sure the loan (or any loan for that matter) complies with the tax rules (“zakelijke lening”): paying interest that conforms to the market, a redemption scheme, and proper collateral (“zekerheden”).

At least to cover your bases when things go awry. Also, the tax authority may conclude a non-conforming loan was in fact an investment (“bodemloze put lening” or “schijnlening") and apply a different tax treatment. If you have a fiscal unity between the IP holding and operating company, this all becomes less relevant.

The idea of the operating company developing the IP, whereas the IP should be held by the holding, requires a solid and defensible mechanism on the basis of which the operating company is reimbursed once the IP is transferred to the holding. This should take place in a business-like fashion, with factors such as the Innovation Box and WBSO to be accounted for.

It would seem the minimum viable structure (let me claim the “MVS” abbreviation here!) to start off is an individual holding per founder and the founders holding. You can then fork off the IP holding as a subsidiary, and from there the operation companies, right?

In principle, you can always split off (“laten uitzakken”) a new subsidiary and transfer the assets there. The assets can be paid in shares or cash. Yet defining and documenting the value of the assets requires some serious black magic voodoo, which is obviously an expensive endeavor. Alternatively, you may want to choose a carve-out of assets in a tax neutral manner (legal demerger, business merger), making the necessity for a valuation less apparent and save tax on the go. Note that such a tax-neutral transaction may become a problem if you would like to sell shares of the new entity going forward. With careful planning when doing the carve-out, your tax advisor can prevent later taxation.

Essentially, you want to avoid all of that, and start off with the right structure. See “the bottom line” below.

The MVS (minimum viable structure) is an individual holding for each founder, an IP holding, and at least one operating company. Lots of legal entities, but hey, at least the notary will love you.

What are your considerations in structuring your startup?

Credits to Sam Abbing from Taxperience for his invaluable tax insights and review; Joris Schreurs and Bas Groot from Halsten Legal, especially on the pains and gains of certificates vs. non-voting shares vs. SARs; Lodewijk Hox from Boels Zanders for his review and dotting the legal i’s, and the CEOs that kindly explained their considerations in setting up their software startup. Cheers!

About Martijn Rutten

Fractional CTO & technology entrepreneur with a long history in challenging software projects. CTO at LUMO Labs impact VC. Former CTO of scale-up Insify, changing the insurance space for SMEs. Former CTO of fintech scale-up Othera, deep in the world of securitized digital assets. Coached many tech startups and corporate innovation teams at HighTechXL. Co-founded Vector Fabrics on parallelization of embedded software. PhD in hardware/software co-design at Philips Research & NXP Semiconductors. More about me.

Related Posts